5 Best Long-Term Buys From Morgan Stanley's 60-Stock Space Race Universe

And no, SpaceX isn't one

With the SpaceX IPO coming to the Nasdaq in the next few weeks I thought it would be interesting to take a look at various names within this industry and determine different ways investors could get some space exposure.

Before we start, I’m not investing in SpaceX when they IPO. I think it’s very likely SpaceX will be a wonderful business long-term however I’m not in at a valuation that could come in between $1.5 to $2 trillion dollars.

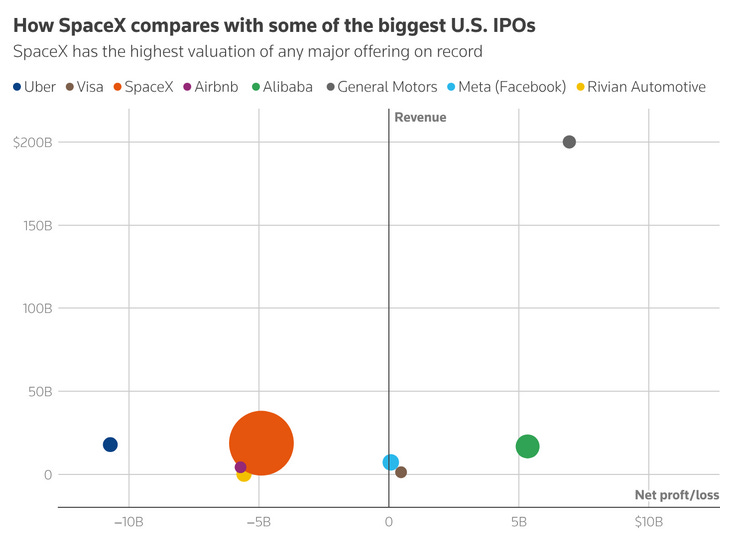

To give you some perspective, this graphic from Reuters illustrates how outrageous the valuation is for SpaceX compared to other significant IPOs:

Now, investors could look at space related ETFs such as the ARK Space & Defense Innovation ETF (ARKX) however not all of these companies are related to the Space industry and some are being pushed up further by the current Iran conflict. Still, ARKX is having a decent year with returns over 18% YTD so it could be an option for investors wanting diversification.

For investors looking for some individual companies, Morgan Stanley has mapped out 60 stocks associated with the space race. These stocks include companies across the supply chain, from rare earths and industrial gases to semis, optics, launch systems and satellite communications.

Sixty is a lot to digest so I’ve reduced the list down to the five top options for long-term investors based on the following criteria:

Founder-led

Unique and differentiated offering

Hard to duplicate offering (i.e. high switching costs)

Under $50 billion in market cap

Growing revenue

Limited LT Debt

I believe these criteria can help deliver market-beating returns for patient long-term investors. That said, here are the top five options:

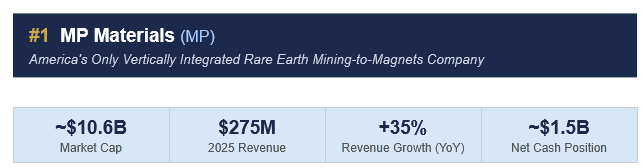

#1 MP Materials (MP)

The Business

MP Materials owns and operates the only rare earth mining and processing facility in the Western Hemisphere capable of producing separated rare earth oxides and magnets at scale. The company has achieved full vertical integration from mining ore in the ground all the way to finished NdPr magnets, which are the essential components in EV motors, defense systems, wind turbines, and consumer electronics.

In 2025, MP Materials nearly doubled its NdPr oxide output to 2,599 metric tons, signed landmark supply agreements with Apple and the U.S. Department of Defense, and launched its Fort Worth, Texas magnetics manufacturing facility — representing a strategic step change from raw material supplier to finished product manufacturer.

Why It Qualifies

1. Founder-Led

✓ James Litinsky — Co-Founder, Chairman, President & CEO

2. Unique & Differentiated

✓ Only mine-to-magnet rare earth company in the US; sole Western supply of NdPr at scale

3. Hard to Duplicate

✓ 10+ years and $billions to replicate; environmental permits, technical expertise, supply chain. China controls 90%+ of global supply

4. Under $50B Market Cap

✓ ~$10.6B — significant runway as rare earth demand scales with EVs and defense

5. Growing Revenue

✓ $275M FY2025 (+35% YoY); magnetics segment (zero in 2024) reached $66.9M; EBITDA turned positive in Q4 2025

6. Limited Long-Term Debt

✓ ~$1.5B in cash; returning to EBITDA profitability; manageable debt relative to asset base

The Investment Thesis

MP Materials is the single most critical infrastructure asset in the US space and defense supply chain. Rare earth magnets (particularly NdPr-based permanent magnets) are irreplaceable in satellite attitude control systems, drone motors, missile guidance systems, and virtually every electric motor used in space vehicles.

The strategic moat is extraordinary: China controls roughly 60-90% of global rare earth processing capacity. The US government has explicitly identified domestic rare earth production as a national security priority. MP Materials is the answer. This isn’t a speculative growth story as it’s a government-backed monopoly on a critical input with no near-term domestic competition.

Litinsky’s vision extends well beyond mining. The Apple contract alone signals that MP can sell finished magnets to the world’s most demanding supply chain customer. DoD contracts further validate the national security angle. As the Fort Worth facility scales, the revenue mix shifts toward higher-margin finished goods, potentially driving EBITDA margins into the 30-40%+ range.

Key Risks

Rare earth commodity price volatility can compress margins in the materials segment

Fort Worth magnetics facility ramp takes time; $500-600M CapEx planned for 2026

China could strategically flood global markets to suppress prices and impede competition

Regulatory and permitting complexity associated with mining operations

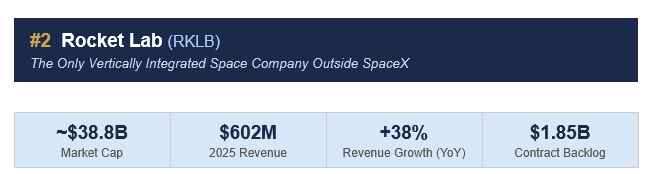

#2 Rocket Lab (RKLB)

The Business

Rocket Lab is the world’s only vertically integrated space company outside SpaceX — designing, building, and launching rockets, while simultaneously manufacturing spacecraft and space systems for governments and commercial operators. The Electron rocket has become the world’s most-launched small orbital launch vehicle, with a 100% mission success rate in 2025. The company’s Space Systems segment now generates the majority of revenue through spacecraft manufacturing, satellite components, and reaction control systems.

CEO and founder Sir Peter Beck is developing Neutron, a medium-class, reusable rocket targeting $50-100M+ missions, with first launch targeted for Q4 2026. If successful, Neutron will position Rocket Lab as a credible competitor to SpaceX’s Falcon 9 franchise.

Why It Qualifies

1. Founder-Led

✓ Sir Peter Beck — Founder & CEO since inception; knighted in New Zealand for services to aerospace

2. Unique & Differentiated

✓ End-to-end space company: launch + spacecraft manufacturing + components. Only such entity outside SpaceX

3. Hard to Duplicate

✓ Launch vehicles require years of certification; spacecraft manufacturing requires classified clearances and mission heritage

4. Under $50B Market Cap

✓ ~$38.8B — approaching threshold but still eligible; Neutron represents significant upside optionality not priced in

5. Growing Revenue

✓ $602M FY2025 (+38% YoY); $1.85B backlog (+73% YoY); Q1 2026 guidance of $185-200M

6. Limited Long-Term Debt

✓ ~$415M in convertible notes offset by $1.1B+ cash — net cash positive ~$685M+; manageable

The Investment Thesis

Rocket Lab has built something that takes 15-20 years to replicate: a proven, certified launch system with mission heritage and government trust. The Electron rocket now flies with a cadence that generates meaningful recurring revenue while the Space Systems segment scales rapidly through government satellite manufacturing contracts.

The $816 million Space Development Agency contract awarded in 2025 to build 18 satellites — announced alongside partnerships with the US military for hypersonic test missions — demonstrates that Rocket Lab has graduated from a launch provider to a full-spectrum space prime contractor. This is the playbook Peter Beck has been executing for years.

The option value in Neutron is substantial. A successful medium-lift reusable rocket would access a market currently served almost exclusively by SpaceX. Even capturing 10-15% of Falcon 9’s annual launch cadence would add $500M+ in annual revenue. At current valuation, the market is not pricing in Neutron success, making RKLB one of the most asymmetric setups in the space sector.

Key Risks

Market cap approaching $50B threshold — may breach if growth continues

Neutron development delay (Q4 2026 target after stage 1 tank test failure) adds uncertainty

Loss-making on a GAAP basis; path to profitability depends on scale and Neutron economics

SpaceX remains a formidable incumbent with lower cost structure

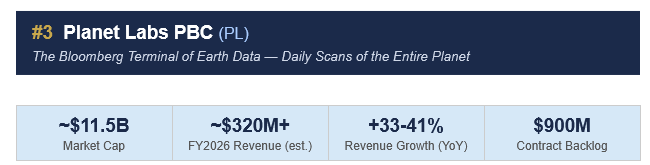

#3 Planet Labs PBC (PL)

The Business

Planet Labs operates the world’s largest Earth observation satellite constellation of over 200 satellites that photograph the entire landmass of Earth every single day. The company sells this imagery through a data-as-a-service platform to governments, intelligence agencies, agricultural firms, financial analysts, climate researchers, and enterprises worldwide. Customers don’t buy satellite images; they buy a continuous, living data subscription to the state of the planet.

Planet’s competitive advantage compounds over time: every day of data adds another layer of historical context that enables analytical models, change detection, and trend analysis that new entrants simply cannot replicate. The company achieved its fourth consecutive quarter of adjusted EBITDA profitability in Q3 FY2026 and its third consecutive quarter of positive free cash flow.

Why It Qualifies

1. Founder-Led

✓ Will Marshall — Co-Founder, CEO & Chairman since 2010; former NASA scientist

2. Unique & Differentiated

✓ Only company with daily global Earth observation at scale; 7+ years of historical data archive unmatched by any competitor

3. Hard to Duplicate

✓ Requires 200+ satellites + years of data history + analytics platform. New entrants need 5-10 years minimum to build comparable archive

4. Under $50B Market Cap

✓ ~$11.5B — significantly undervalued relative to the data platform opportunity

5. Growing Revenue

✓ FY2026 Q4 revenue +41% YoY to $86.8M; $900M backlog (+79% YoY); FCF turned positive

6. Limited Long-Term Debt

✓ $460M convertible notes offset by $677M cash — net cash positive ~$217M; stable

The Investment Thesis

Planet Labs has quietly built the infrastructure layer for Earth intelligence. In the space economy, the most durable businesses will not be rocket companies, they will be the companies that own the data streams that flow from space to Earth. Planet’s daily global imagery is already embedded in critical government intelligence workflows, agricultural insurance models, and financial risk assessments.

The switching cost is not just technical, it is temporal. Seven-plus years of daily satellite imagery creates a historical dataset that forms the baseline for all change detection, environmental monitoring, and predictive analytics. A customer who has built models on Planet’s data cannot simply switch to a competitor without losing years of calibration. This is the deepest moat in the space data sector.

The business is transitioning from a pure imagery company to a full analytics platform, adding AI-driven analysis layers on top of the raw data. This mirrors the evolution of Bloomberg from a data terminal to an analytical platform and suggests significant pricing power as Planet moves up the value chain. With the backlog surging 79% and FCF turning positive, the inflection is already underway.

Key Risks

$460M in convertible debt creates some dilution risk if stock price does not perform

Increasing competition from government-backed programs (e.g., European Copernicus) and new commercial entrants

Revenue concentration in U.S. government contracts creates budget cycle sensitivity

Satellite constellation requires ongoing CapEx for replacement and expansion

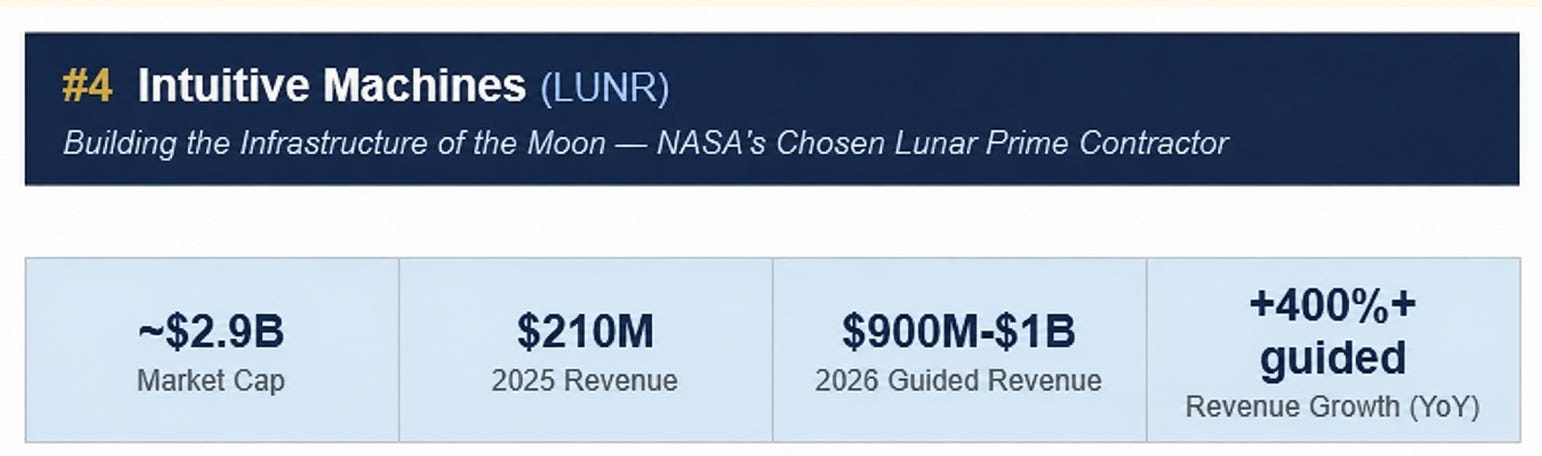

#4 Intuitive Machines (LUNR)

The Business

Intuitive Machines is America’s premier commercial lunar services company, having achieved the first US soft landing on the Moon since 1972 (IM-1 mission, 2024) and the first targeted landing near the lunar south pole (IM-2 mission, 2025). Beyond lunar landing, the company is building the Near Space Network — a communications relay and data infrastructure architecture for cislunar space and is rapidly expanding into national security space programs.

The acquisition of Lanteris Space Systems (Q1 2026, $800M) and KinetX Aerospace (2025) has transformed Intuitive Machines from a lunar specialist into a full-spectrum space prime contractor with capabilities in navigation, mission design, and national security satellite operations. The 2026 guidance of $900M-$1B represents a 5-6x revenue increase — one of the most aggressive growth ramps in the sector.

Why It Qualifies

1. Founder-Led

✓ Steve Altemus — Co-Founder, President & CEO; 10% owner; former NASA JSC Deputy Director

2. Unique & Differentiated

✓ Only proven commercial lunar lander in the US; building Near Space Network — the ‘internet of the Moon’

3. Hard to Duplicate

✓ Lunar landing heritage takes decades; NASA relationships built over 10+ years; classified national security contracts require clearances and trust

4. Under $50B Market Cap

✓ ~$2.9B — extraordinary upside potential if $900M-$1B 2026 revenue guidance is achieved

5. Growing Revenue

✓ $176M (2025) → $900M-$1B guided (2026); NASA Artemis program and national security expansion driving step-change growth

6. Limited Long-Term Debt

✓ $335M convertible debt, $582M cash — net cash positive; Lanteris acquisition was primarily stock-based

The Investment Thesis

Intuitive Machines is best understood as the AWS of cislunar space. Just as Amazon Web Services built the infrastructure layer that enabled the cloud economy, Intuitive Machines is building the navigation, communications, and logistics infrastructure that will enable permanent human and robotic presence on the Moon.

The Near Space Network which is providing positioning, navigation, and data relay services beyond low Earth orbit has no commercial analog. It is the functional equivalent of a space internet backbone for the lunar economy. Once governments and commercial operators begin relying on this network for mission-critical operations, switching costs become prohibitive.

At ~$2.9B market cap against $900M-$1B in guided 2026 revenue, the valuation is remarkably undemanding if execution materializes. Steve Altemus has skin in the game (10% ownership) and a deep institutional knowledge of NASA’s requirements from his time as JSC Deputy Director. The Lanteris acquisition accelerates the timeline to becoming a full-spectrum national security space prime — a market that dwarfs commercial lunar services.

Key Risks

$800M Lanteris acquisition is large relative to company size and integration risk is real and significant

Revenue guidance depends on execution of multiple complex government programs simultaneously

Lunar mission failures would severely damage the brand and NASA relationship

National security contracts require sustained political and budget support

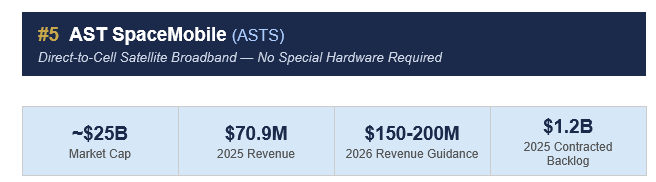

#5 AST SpaceMobile (ASTS)

The Business

AST SpaceMobile is attempting something genuinely unprecedented: delivering broadband internet directly to standard, unmodified smartphones via a constellation of large low-Earth orbit satellites. No dongle, no special phone, no separate subscription device, just your existing AT&T or Verizon handset connecting to a satellite in space. The company successfully demonstrated the first-ever direct-to-cell video calls and RCS messaging using standard 850 MHz spectrum in late 2025.

The business model is elegant: AST charges mobile network operators (MNOs) a 50/50 revenue share on ‘space roaming’ subscriptions — an add-on to existing cellular plans. AT&T, Verizon, Rakuten, Vodafone, and 45+ other MNO partners have signed agreements. The 2026 revenue guidance of $150-200M reflects initial commercial service; CEO Abel Avellan has outlined a path toward ~$1B in annual revenue by 2027 as the satellite constellation scales.

Why It Qualifies

1. Founder-Led

✓ Abel Avellan — Founder & CEO; previously sold Emerging Markets Communications for $550M

2. Unique & Differentiated

✓ First and only company to achieve direct-to-cell broadband from space using standard smartphones; years ahead of any true competitor

3. Hard to Duplicate

✓ Requires massive satellite constellation + licensed cellular spectrum + exclusive MNO partnerships + regulatory approvals in 50+ countries

4. Under $50B Market Cap

✓ ~$25B — significant upside if revenue ramp toward $1B+ materializes

5. Growing Revenue

✓ $70.9M (2025) → $150-200M guided (2026); 2,731% Q4 2025 YoY growth rate; $1.2B contracted backlog

6. Limited Long-Term Debt

~ $2.2B in convertible notes offset by $2.8B in cash — net cash positive, but debt is elevated for current revenue scale

The Investment Thesis

The total addressable market for universal mobile connectivity is measured in the hundreds of billions of dollars. There are roughly 5 billion smartphone users worldwide, and over 1 billion people live in areas with no or limited cellular coverage. AST SpaceMobile does not require them to buy new hardware as it works with the phone already in their pocket.

The strategic advantage is reinforcing: MNO partnerships create revenue share arrangements that align large telecoms with AST’s success. AT&T and Verizon cannot easily switch to a competitor because their existing customers are already enrolled in space roaming plans. As the constellation grows from initial BlueBird satellites toward a full network, coverage gaps close and the value proposition strengthens.

Avellan has demonstrated he can build and sell satellite companies (EMC, sold for $550M). He has done this before. The key risk to monitor is the pace of satellite deployment versus the burn rate — but with $2.8B in cash and $1.2B in contracted backlog, the runway is sufficient to reach revenue scale. The debt is a concern but is structured as long-duration convertible notes, minimizing near-term cash pressure.

Key Risks

$2.2B in long-term debt is the most significant blemish on the investment case so monitoring is required

Satellite deployment costs are enormous; any delay or failure could extend the path to cash flow breakeven

Starlink (SpaceX) is developing direct-to-cell capabilities, though requires satellite-enabled devices

Regulatory complexity across 50+ countries creates licensing risk and deployment delays

Conclusion

I think all five are very interesting stock picks that could delight investors in the years (and perhaps decades) to come. Of the five, I’d say I have the highest conviction in Rocket Lab despite the fact it’s going head to head with SpaceX. I don’t think it will be a winner take all scenario thus why if I was going to place a bet on one of these five it would be Rocket Lab.

Do you have a favorite of these five or another company you believe will be a beneficiary of the space race? If so, please share in the comments section below.

I don’t do well speculating on individual companies in hot sectors, but I do have some XAR because I do think aerospace and defense is a very solid sector overall. Nice write up as always! I’m sure I’ll be an investor in some of these companies in 20 years lol