Deep Dive - TransMedics - A Growing Innovator in a Niche Industry

Recent Pullback Creates An Opportunity for Long-Term Investors

As my readers will know, I’m a big believer in companies where leadership has skin in the game. Additionally, I like to invest in growing industries and those with competitive advantages. TransMedics Group, Inc. hits on all of those which is why it’s one of highest conviction holdings.

Despite, Transmedics struggling thus far in 2026, I fully believe this company will be a winner for patient long-term investors.

Let’s dig in!

The Company

TransMedics Group was founded in 1998 by Waleed Hassanein, a physician with a medical degree from Georgetown University who has dedicated his career to solving one of medicine’s most persistent logistical problems: getting healthy donor organs to patients who need them.

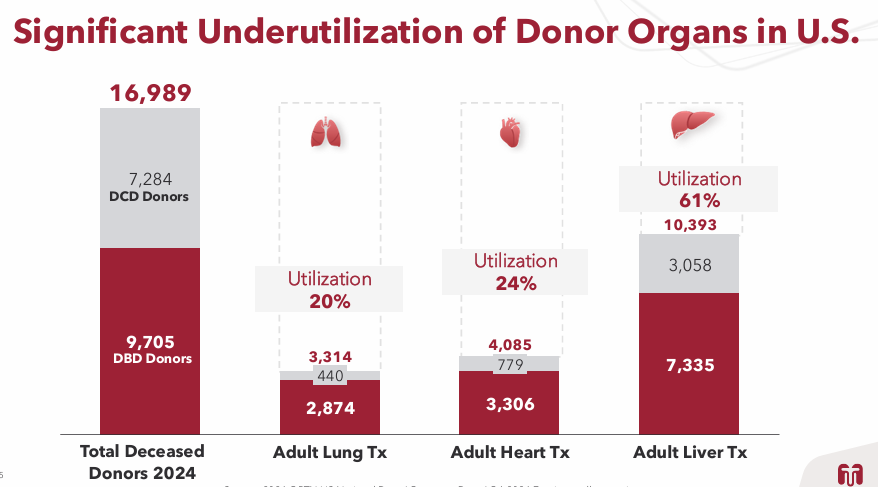

For decades, the standard method of organ preservation and transport has been static cold storage (SCS). Cold storage works, but it introduces serious limitations. By depriving an organ of oxygen, it creates a narrow window of viability that limits how far the organ can travel from donor to recipient. The result is a system that consistently underutilizes available donor organs, leaving thousands of viable transplants on the table every year.

The graphic below illustrates the significant underutilization of donor organs in the United States:

TransMedics developed a fundamentally different approach. Their Organ Care System (OCS) preserves and transports organs by perfusing them with warm, nutrient-enriched blood, recreating the conditions of a functioning human body. The heart keeps beating. The lung keeps breathing. The liver keeps functioning. By maintaining the organ in a near-normal physiologic state, the OCS dramatically extends the window of viability and enables transplant teams to work with organs that would have previously been rejected.

Clinical trials have consistently demonstrated superior outcomes with the OCS compared to cold storage, and the platform currently supports heart, lung, and liver transplants. Most importantly, the OCS is the only FDA-approved multi-organ warm perfusion platform in the world.

This type of technology already gives TransMedics a leg up on the competitor but let’s next get into the “TransMedics Trident” which further adds to the company’s moat.

The Competitive Moat: The TransMedics Trident

When thinking about TransMedics’ competitive position, it helps to picture a trident with three reinforcing prongs: the OCS technology itself, the National OCS Program (NOP), and a dedicated logistics and aviation network. Together, these three elements create a moat that is extremely difficult for competitors to replicate.

The OCS technology is protected by roughly 400 worldwide patents and pending applications. Two competitors, OrganOx Limited and XVIVO Perfusion AB, have developed warm perfusion systems of their own, but neither holds FDA approval for a multi-organ platform. That regulatory gap gives TransMedics a head start that takes years to close.

The National OCS Program brings the second prong to life. Through the NOP, TransMedics provides transplant centers with trained organ procurement surgeons, clinical specialists, and transplant coordinators, creating an end-to-end solution that goes well beyond selling a device. The NOP has grown significantly since inception and now represents a meaningful portion of the company’s service revenue.

The third prong is the dedicated logistics network. TransMedics acquired Summit Aviation in August 2023 to address a persistent bottleneck in their operations. Prior to the acquisition, the company had relied on charter flight brokers, encountering problems with older planes, fragmented operators, unreliable availability, and inefficient routes. With an owned fleet, TransMedics controls the quality and efficiency of organ transport in a way that no broker arrangement could match.

The combination of these three elements is what makes TransMedics so difficult to displace. A competitor can build a competing perfusion device, but they cannot simply replicate the NOP infrastructure, the trained clinical staff, and the dedicated air and ground network that TransMedics has spent years constructing.

While not part of the Trident, I think it’s worth noting Waleed Hassanein has remained the company’s CEO and as of the company’s latest proxy statement held over 4% of all shares beneficially owned. Skin in the game is something I look for because like shareholders, CEOs and founders with stock have an incentive to grow the business while maintaining that long-term focus.

A Growing Pipeline of Catalysts

One of the most compelling aspects of the TransMedics story is the runway still ahead in terms of new products and platform expansion.

TransMedics is currently developing next-generation OCS offerings for heart and lung. The ENHANCE program targets the heart OCS and the DENOVO program targets the lung OCS. Enrollment in both clinical programs should be underway shortly, and management has indicated that all FDA questions and IDE conditions are expected to be satisfied in the months ahead.

Beyond next-generation updates to existing platforms, TransMedics is working on OCS Kidney, which would add a fourth organ to the company’s portfolio. On the latest earnings call, Hassanein called the 10,000 transplant goal by 2028 essentially a slam dunk, and then went further, suggesting that with the addition of kidney transplants, the company could be looking at 20,000 transplants by 2030. That figure is extraordinary relative to the approximately 2,300 OCS transplants that occurred in the United States in 2023, illustrating just how early in the adoption curve we still are.

When asked about where additional market penetration will come from, specifically in liver, Hassanein was unequivocal: “We think we are early in our liver penetration, and we have a long greenfield opportunity in liver transplant to grow our adoption rate over the next several years...We are very, very much believers that the notion that growth in liver is going to be difficult to come by is a false assumption, propagated by the wrong narrative.”

This quarter also introduced a new offering to the portfolio: the TransMedics Controlled Hypothermic Organ Preservation System, or CHOPS. CHOPS offers a cost-efficient complement to the OCS for situations where full warm perfusion is not necessary.

Beyond new donor organs and offerings, TransMedics is also expanding internationally. TransMedics is actively building four OCS hubs in Italy as part of the first European NOP program. Additionally, TransMedics is working on establishing NOP locations in the Netherlands and Belgium. And to support the European logistics network, the company recently signed an agreement with PAD Aviation, a charter flight operator based in Germany that uses the same model aircraft as the domestic fleet. Hassanein described the vision: "Simply stated, we're planning to replicate the success of the U.S. NOP in Europe to potentially expand or nearly double our total addressable market, increase OCS clinical adoption and provide efficient and dedicated transplant logistics service across Europe using our dedicated logistics network."

Despite the positives, there are risks associated with TransMedics which we can get into next.

Risks

Regulatory approval and compliance remain the highest-order risk for the business. TransMedics must obtain and maintain approvals from the FDA and from international regulatory agencies. Any unforeseen issues with the ENHANCE, DENOVO, or OCS Kidney programs could delay their launch timelines and push out the growth catalysts that underpin the longer-term bull case.

Execution risk around the European NOP is also worth acknowledging. The Italian program represents the first time the company is building this infrastructure outside the United States. A stumble in Italy could slow engagement with other European countries and temper the broader international opportunity.

Seasonality is a lower-stakes but real consideration. TransMedics can see notable quarter-to-quarter fluctuations, and investors should be prepared for quarters that may look softer due to seasonal patterns (often due to weather) rather than underlying demand weakness.

Financials

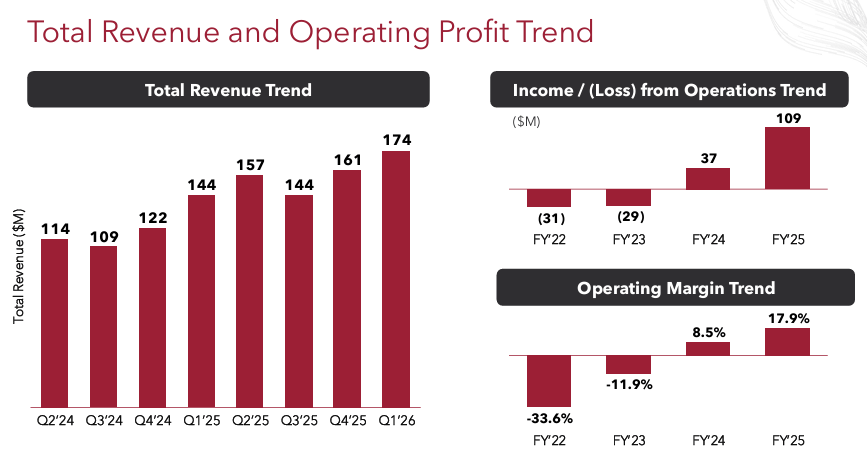

Before jumping in Q1 2026, I always like to take a step back and look at the big picture. You can clearly see below that revenue has been growing and operating margins have improved over the last few years despite large expenditures associated with growth initiatives:

In Q1 2026, TransMedics generated revenue of roughly $173 million, which is an increase of 21% compared to Q1 2025. Breaking it down by organ, you can see in the graphic below that liver continues to account for most of the company’s revenue and has been the leading driver of the company’s growth, as liver revenue grew by over 27% year-over-year and nearly 9% quarter-over-quarter:

Breaking out the $173 million, product revenue for the quarter was $102 million, an increase of 22% compared to Q1 2025. Service revenue came in at $66 million, which is a 19% increase year-over-year. Both clinical service revenue and logistics revenue continue to drive service revenue growth, as you can see below:

Despite this revenue growth, increases in the total cost of revenue and operating expenses led to a decline in net income and earnings per share, as you can see below:

This earnings miss led to the significant downward move in the company’s stock price.

On the earnings call, management noted that R&D increases were due to continued development of their OCS kidney platform and the company’s next-generation OCS offerings. Additionally, there were further costs associated with the DENOVO and ENHANCE programs plus the costs associated with supporting the expanding NOP efforts.

Management reiterated their full-year 2026 revenue guidance, which is $727 to $757 million. That would represent a 20% to 25% increase in revenue from the prior year. Management is also expecting long-term gross margins to be around 60%. In the current quarter, gross margin was 58%.

Lastly, higher fuel costs did impact the company’s operating expenses as well. Management didn’t give a figure but stated they were “doing right by our customers,” so I’d assume they are eating some, if not all, of the added expense.

Moving on to the company’s balance sheet, TransMedics has a cash balance of $461 million and more than enough current assets to cover all of their current liabilities, as you can see below:

Valuation

After the selloff, TransMedics looks attractively priced relative to its own history. The company’s forward price-to-sales ratio has dropped sharply compared to earlier this year, and the current TTM price-to-sales ratio is now below the company’s five-year historical average. For a business still compounding revenue at 20% or more annually, that compression is notable.

From another viewpoint, in using my reverse discounted cash flow model, using the company’s latest cash flow figures (LTM) with a discount rate of 10% and a terminal rate of 3%, TransMedics would have to grow at a mere 4% to justify today’s stock price:

Based on the current analyst estimates, it seems like the current sentiment is that TransMedics can easily grow beyond 4%, as most think it’s going to grow by double digits over the next several years. I, for one, think TransMedics will surely grow beyond 4% given international expansion, OCS kidney, next-generation offerings, and perhaps the inclusion of even more organ offerings.

Conclusion

TransMedics is down sharply from its highs, but the long-term thesis has not changed. The company is still the only operator with an FDA-approved multi-organ warm perfusion platform, a vertically integrated logistics and aviation network, a growing national program, and now a rapidly developing international presence. The pipeline of new products including Kidney OCS, ENHANCE, DENOVO, and CHOPS gives the company multiple levers to pull for growth over the next several years.

The earnings miss in Q1 2026 created a painful dislocation, but the revenue growth continues, the full-year guidance was maintained, the balance sheet is strong, and management remains fully invested in the outcome of this business.

For high-quality growth companies, volatility is often the price of admission. TransMedics, in my view, falls squarely in that category. I’m a believer in this business and think investors buying at these levels could be rewarded in the years to come.

This article is for informational purposes only and does not constitute financial advice. All investments carry risk. Please do your own due diligence before making any investment decisions.

This is a very interesting company that I keep hearing about! Not my cup of tea but something I’ll keep an eye on!

Very interesting company, didn’t know about them. Thank you