Procore - Turnaround Potential for this SaaSpocalypse Victim

Niche tech construction player has potential with AI

Like many SaaS players, 2026 has been a rough year for Procore Technologies. Yet, this business finds itself in the driver’s seat in a niche market, one that potentially will have the AI capabilities to keep their steady and growing customer base happy. However, some significant risks remain such as the previously founder and CEO recently stepping aside.

Let’s dive into Procore as I discuss tailwinds as well as challenges for this business.

The Company

Procore Technologies (PCOR) was founded back in 2002 by Craig “Tooey” Courtemanche. At the time Courtemanche was working in Silicon Valley but had a house being built in Santa Barbara. Courtemanche was having various issues surrounding the communication of the job with the numerous parties involved and so Courtemanche created a way in which all these parties could communicate with one another more effectively and thus Procore was born.

The company’s mission is simple, “To connect everyone in construction on a global platform.” Procore is the leader in providing cloud-based construction management software. The construction industry is a complex one with many key players depending on the job or task at hand. Procore’s technology helps connect those involved in a construction job such as owners, general and specialty contractors, architects, and engineers so tasks can be completed in a timely and efficient fashion.

In today’s SaaS market, I think it’s worth mentioning that Procore is not a seat-based SaaS company. Most construction software charges per user. Procore does not. Their pricing is based on Annual Construction Volume, or ACV, which is the annualized dollar value of projects a customer manages on the platform. Subscriptions are fixed-fee and renew annually or on multi-year terms.

AI Is the Story, but the Rollout Is Deliberate

One big recent development is the January 2026 acquisition of Toric Labs, Inc., better known as Datagrid, for $168 million in cash. Datagrid specializes in agentic AI solutions purpose-built for the construction industry, and the deal is a clear signal that Procore is serious about embedding AI across its platform.

One early example of AI worth highlighting is that an enterprise customer called Crest Operations used Procore AI to compress a manual, multi-week bidding process down to twenty minutes. That kind of operational change is exactly what construction firms need, and it illustrates the genuine productivity upside AI can deliver in this space.

CEO Ajei Gopal framed the opportunity this way on the Q1 call:

“When you talk to customers, many of them don’t really have the time or the inclination to become experts in AI and construction. They look to us as being their technology partner. They’ve worked with us for years. They trust us. And their objective is they just want to be able to build better projects.”

That customer dependency is a structural advantage. Construction firms tend to outsource technology decisions rather than build capabilities in-house, which means Procore has an embedded, trusted position that is difficult for a competitor to displace. If the AI tools prove genuinely useful, adoption should follow naturally.

That said, the rollout has been intentionally slow. Procore currently operates with a small dedicated AI team working alongside the broader sales force. Management made this choice deliberately to learn directly from customers before scaling. A larger rollout is expected in Q3 2026. The measured pace is strategically sound, but it means margin compression from AI-related costs will show up before meaningful AI revenue arrives.

Procore also announced a partnership with Nvidia in Q1 to accelerate the building of AI data centers and infrastructure. As hyperscaler construction spending remains robust, this is a useful strategic tie-in.

Risks

Management Turnover - One factor that does not always get enough attention is the composition of the leadership team. Procore founder Craig “Tooey” Courtemanche Jr. remains Chairman of the Board and still holds approximately 4% of outstanding shares, which is a genuine positive. Founders with meaningful ownership tend to keep the long-term in view.

But the day-to-day team has changed significantly. Ajei Gopal is now CEO, and while his background is strong, it is simply too early to assess his track record in this role. Procore has also brought in a new CFO, Rachel Pyles, and a new Chief Revenue Officer, Walt Hearn, who joined in April. Three key seats turning over in a relatively short window introduces execution risk, not because any of these individuals are unqualified, but because organizational alignment and investor trust take time to build. The next few quarters will matter a great deal in answering the question of how this team performs under pressure.

Macro and Cyclicality - Procore's revenues rise and fall with construction activity. Interest rates affect housing starts and commercial development, tariffs affect the cost of building materials, and geopolitical uncertainty can pause capital allocation decisions across the industry. Management noted a relatively stable macro environment in Q1, with optimism around data center construction in particular. But the underlying sensitivity to construction cycles is structural, not temporary, and the current environment remains uncertain.

AI Adoption - The construction industry has historically been slow to adopt new technology. Management acknowledged this directly on the Q1 call, noting that the dedicated AI team is small and the broader rollout is still months away. If customers prove reluctant to adopt AI agents at scale, the AI-related costs hit the income statement before any offsetting revenue arrives. Management has explicitly flagged near-term AI cost headwinds to margins. If adoption lags, the path to profitability extends.

Financials

In Q1 2026, Procore reported sales of $359 million, which is an increase of 16% compared to Q1 2025. Gross margins remained strong, coming in at 80% for the quarter (GAAP). However, the business remains unprofitable as total operating expenses continue to rise, led by an increase in sales and marketing expenses:

The company’s net loss this quarter did shrink compared to Q1 2025, but shareholders continue to see stock dilution as total weighted-average shares outstanding increased year-over-year.

Moving on to important company metrics, Procore now has 2,795 customers contributing more than $100,000 in annual recurring revenue, which is a 16% increase year-over-year. The company continues to maintain its impressive gross revenue retention rate of 95% for the quarter. Free cash flow was $56 million, an increase of 20% compared to Q1 2025. Lastly, current RPO and current deferred revenue grew by 21% and 17%, respectively, compared to the prior year’s first quarter.

In Q2 2026, Procore is predicting revenue in the range of $364 to $366 million, which represents YoY growth of 12% to 13%. For the full fiscal year, Procore raised their guidance and are now expecting revenue in the range of $1,499 million to $1,503 million, which is more than a 13% increase compared to fiscal year 2025. Free cash flow margin is expected to be 19%.

Procore continues to have a solid balance sheet, as the company has more than enough current assets to cover all the company’s current liabilities. Procore’s current cash balance is $386 million, which is down compared to the $480 million as of December 31, 2025, but the company has been using cash for M&A as well as share buybacks. In Q1 2026, Procore repurchased roughly 1.8 million shares for approximately $100 million.

Valuation

Shares recently traded near $49, putting the market cap at approximately $7.5 billion. That prices Procore at roughly 5.0x forward revenue on the FY2026 guidance midpoint of $1.5 billion, and about 5.4x trailing twelve-month revenue. For a software business with 80% gross margins, 16% revenue growth, and a 95% gross retention rate, that is a historically modest multiple. At peak valuations in 2021, this stock traded above $140 and commanded multiples above 30x revenue. The market has clearly recalibrated its expectations, and the question now is whether the current price reflects fair skepticism or overdone pessimism.

A few lenses help frame the answer.

On a free cash flow basis, the picture is more nuanced. Management guided for a 19% FCF margin in FY2026, which would imply roughly $285 million in free cash flow for the year. At the current market cap, that works out to approximately 26x forward free cash flow. That is not cheap in absolute terms, but it is reasonable for a business with Procore’s retention profile and contracted revenue backlog, particularly as FCF margins continue to expand.

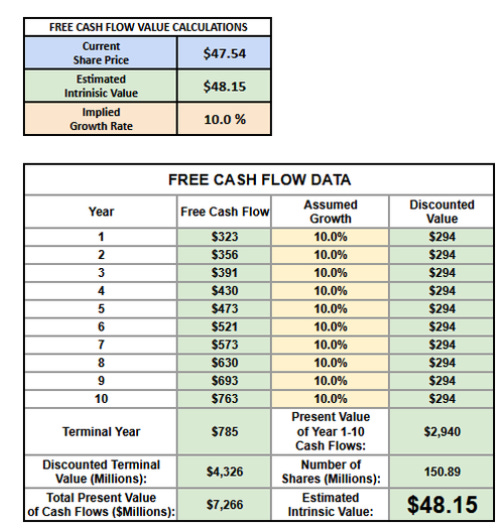

A reverse discounted cash flow model offers another angle. Using the latest trailing free cash flow figure, a 10% discount rate, and a 3% terminal growth rate, the stock is pricing in roughly 10% annual growth:

Management is guiding for 13% this year, and Wall Street consensus sits at 12% to 13% over the next several years. In other words, the current stock price demands less growth than the company itself is projecting, which builds in a small margin of safety. If the AI rollout lifts growth back toward the mid-teens or beyond, the valuation case strengthens considerably.

Lastly, it is also worth considering what the stock scores on the Rule of 40, a widely used SaaS health benchmark that adds revenue growth rate to free cash flow margin. At roughly 14.5% growth plus 19% guided FCF margin, Procore scores around 34, just below the 40 threshold that typically signals a high-quality software business. Crossing that line cleanly, which is achievable with modest acceleration, would likely attract a broader set of institutional buyers and support multiple expansion.

Conclusion

Procore is making strides to enhance their AI offerings, and their acquisition of Datagrid illustrates the company’s commitment to this long-term strategy. While monetization is occurring, the Procore AI rollout has been slow as the company works with customers to find the best ways to create AI efficiencies. Until more monetization occurs, margin compression will likely continue to cut into bottom-line profits.

There is also the question of how this new management team will perform and if they’ll be able to execute.

While I think Procore is fairly valued, if not undervalued, I’ll hold tight for now as I’d like to see how this management team performs for a few quarters and hopefully see more customers adopt the company’s AI solutions.

This article is for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Very interesting! I appreciate how you covered management turnover and ownership and their business not being based on seats is very good. Nice write up CQ!