Remitly: Moving Money, Moving Markets

Now A Profitable Business With Numerous Growth Accelerators

Lately I’ve been on the hunt for some intriguing small and mid-cap stocks and I came across one founder-led business that recently turned profitable and has an growing TAM. That company is Remitly Global.

Let’s dig into the details of this organization as I discuss new growth initiatives, recent financials, and lastly valuation.

The Business

In 2011, Matt Oppenheimer was living in Kenya when he noticed something that troubled him. Immigrants trying to send money back home to their families were getting crushed by fees, delays, and a system clearly designed for the benefit of the middleman rather than the people who needed it most. He knew technology could fix it. Back in the U.S., he connected with fellow co-founders, Josh Hug and Shivaas Gulati, both of whom had family abroad and had seen the same problem firsthand. Together, the three of them founded Remitly.

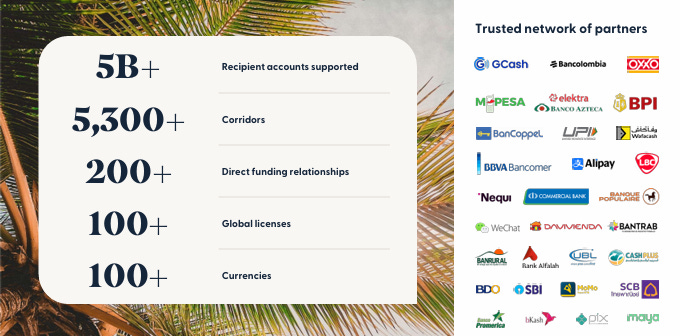

Fifteen years later, Remitly (RELY) serves 9.6 million quarterly active customers across more than 170 countries and over 5,500 send/receive corridors. The company's vision is to "transform lives with trusted financial services that transcend borders.”

Remitly operates a digital-first remittance platform that allows customers to send money internationally through its mobile app and website. Revenue is generated primarily through transaction fees and foreign exchange spreads on cross-border payments.

Remitly’s network has best-in-class speed compared to peers as 63% of transfers occur in less than 20 seconds and 94% occur in less than an hour. Of these transfers, 97.5% of them occur with no need for customer support.

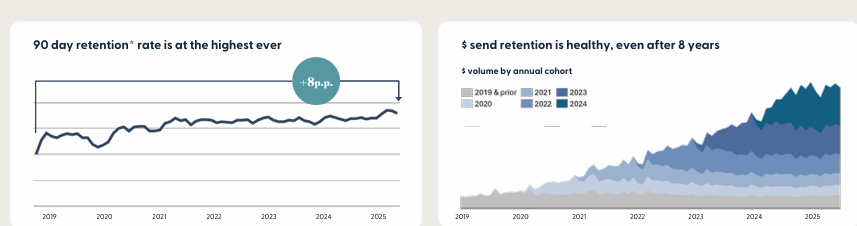

What is impressive as well is that Remitly’s customers are staying with them as evidenced by these retention metrics:

Moat and Opportunities

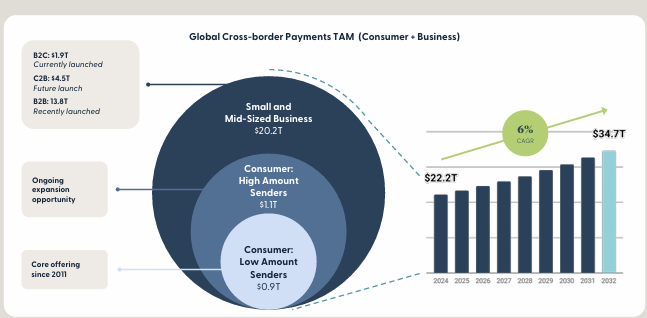

While Remitly is a trusted financial services partner, the company believes they have a $20 trillion TAM with much of that revenue possibly coming from small and mid-size businesses:

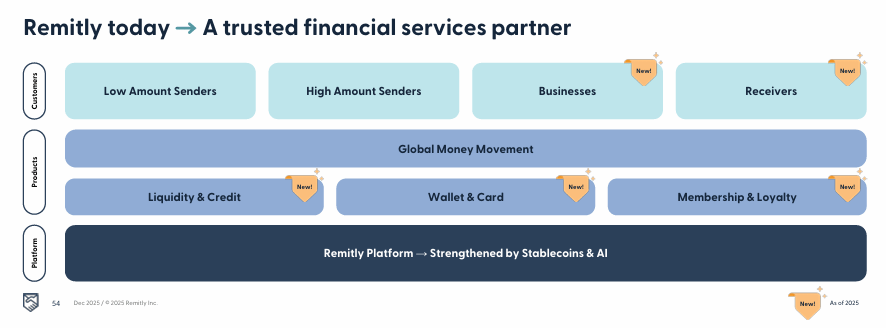

The business has primarily focused on low amount senders but is now moving to high amount senders (sending $5,000 or more per transaction, businesses, and receivers:

The company’s new CEO, Sebastian Gunningham, recently discussed Remitly’s new initiatives when describing the business’s four categories: core senders (low amount senders), high amount senders, businesses, and receivers. When talking about these four categories on the company’s Q1 earnings call, here is what Gunningham had to say:

For each of these customers, we are grouping 4 categories of product offerings, broadly defined around sending money, borrowing money, spending money and saving money. At the intersection of the 4 customer and product categories are many unique opportunities to serve our customers with products they need to live their cross-border financial lives. Each customer category and product offering reinforces the others, drawing on shared infrastructure and data to create compounding benefits as we scale.

Low amount senders have been Remitly’s bread and butter customers historically. Regarding this category, the business has recently completed integrations with WhatsApp and ChatGPT to continue to enhance global reach. The company is also launching Send Now, Pay Later. Within this plan, customers get a global debit card to spend, a wallet to save, and a short-term line of credit offered by a bank partner. Currently, the company is rolling out Send Now, Pay Later just in the United States.

Moving on to high value senders (sending $5,000 or more per transaction), the YoY volume has grown by 73%. Remitly is focused on making setup easier for these customers to streamline transaction efficiency.

Business volume grew 30% compared to the prior quarter and in the quarter the company added five more countries to the list of countries that can request and receive payments. Currently, 26 countries across Latin America and Asia can request and receive payments using Remitly.

Clearly, there is a lot to like as Remitly continues to increase their number of customers (including more high value senders), businesses, and receivers.

Management

Matt Oppenheimer co-founded Remitly and served as CEO since inception, guiding the company from a small startup to a publicly listed fintech with nearly $1.8 billion in annual revenue run rate. He stepped down in early 2026 and was succeeded by Sebastian Gunningham, who brings deep technology and operations experience.

Oppenheimer’s legacy is notable as he built a mission-driven company without losing commercial discipline, and the profitability inflection now underway is a direct result of the operating infrastructure built under his tenure. Investors should monitor Gunningham’s first full year closely for signs of strategic continuity or drift, particularly around geographic expansion priorities and the push into business payments.

As a positive note, Remitly has an active $200M share repurchase program, with $131.9M remaining as of Q1 2026. To me that’s a signal from the board and management that they believe the stock is undervalued relative to intrinsic value. Also, according to the company’s latest proxy statement, Oppenheimer and Josh Hug both hold roughly 2% of all outstanding shares. While I like founders with continued skin in the game, a key management transition always leaves me cautious. I do believe Gunningham seems capable considering his prior experience at Amazon but time will tell.

Risks

No investment is without risk, and Remitly carries several worth taking seriously.

Immigration policy - This is the most significant risk I’d say for Remitly as a meaningful portion of U.S.-originating send volume comes from immigrant communities, including undocumented individuals sending money to families abroad. A sustained or escalating crackdown on the undocumented population could meaningfully impair send volume from the U.S. Remitly is actively diversifying its geographic send base (non-U.S. send revenue is now 34%) but immigration policy remains the single largest watch item for investors.

Regulatory and licensing complexity - Operating across 175+ countries means navigating an ever-evolving patchwork of money transmission laws, AML requirements, and payment regulations. A license suspension in a major corridor or a material compliance failure could be painful and costly.

CEO transition - As I mentioned above, founder Matt Oppenheimer recently stepped down as CEO, replaced by Sebastian Gunningham. Founder departures carry real execution risk as culture, institutional knowledge, and long-term vision are difficult to transfer cleanly. The transition is still early, and investors should monitor whether strategic momentum holds under new leadership.

Competition - I believe competition is intense in this space with numerous competitors like Western Union, MoneyGram, PayPal, Wise, and numerous other players. While Remitly has always been a digital-first company, AI enhancements now make it easier for more of the brick and mortar companies like Western Union, to catch up.

Financials

Before jumping into current quarter results, I want to zoom out to show how Remitly has steadily been growing revenue and revenue less transaction expense over the last few quarters:

In Q1 2026, Remitly generated revenue of roughly $453 million which is an increase of over 25% compared to Q1 2025. Active customers came in at 9.6 million which is an increase of 20% compared to the prior year quarter and send volume increased to $22.1 billion which is up 37% YoY.

Zooming out to look at both send volume and quarterly active customers, both have continued to grow at a double-digit pace over the last several quarters:

While total costs and expenses have increased YoY, Remitly’s revenue growth has far outpaced these costs, resulting in large increases in net income and EPS compared to Q1 2025:

After this solid quarter management is raising their full year guidance. Management is now expecting revenue in the range of $1.96 to $1.975 billion up from the previous guidance of $1.94 to $1.96 billion. Adjusted EBITDA is now expected to be in the range of $370 to $385 million compared to the previous guide of $340 to $360 million.

Remitly still has an excellent balance sheet as you can see below with more than enough current assets to cover all of the company’s liabilities and no long term debt:

Valuation

Despite recently becoming profitable, since Remitly is a high growth business, I maintain that price to sales is likely the best valuation metric for this company.

As you can see below, while the company’s P/S ratio has increased over the last few months, it’s still well below both the sector median and the highs reached in late 2024, early 2025:

From another viewpoint, in using a reverse discounted cash flow model with a discount rate of 10% and a terminal rate of 3%, Remitly would need assumed growth of roughly 6% to justify the current share price:

Wall Street analysts seem to think Remitly can continue to grow by double digits over the next several years, and I would concur given the numerous growth opportunities for the business.

Furthermore, from a ratings perspective, Wall Street analysts are bullish on the stock, predicting continued upside for the stock as you can see below:

Conclusion

I’m bullish on Remitly considering the ongoing initiatives to acquire and retain more customers, especially high value senders. Also, I think the business category could be a huge driver for future growth as Remitly continues to expand into more countries.

The biggest risk to me is the new CEO as a change in senior management always gives me pause. For that reason, I’m keeping a watchful eye on this business but I believe there is certainly much to like with this business.

This article is for informational and educational purposes only and does not constitute financial advice. Always do your own due diligence before making investment decisions.

What are you thoughts on Remitly? Comment below